Order fulfillment and fund are the top two challenges facing e-commerce businesses, our partnership solves these challenges at once. Boxful Fulfillment handles your online store orders, inventory and shipments while Choco Up offers a novel financing solution to e-commerce newbies and SMEs. Let’s take a look at how Choco Up’s financing solution is going to be the best option to start or grow your business.

The Ultimate Guide to Inventory Financing

For retailers, wholesalers and other product-based companies, spikes in demand for your product perhaps create a ‘happy problem’. Financing bulk purchases of inventory could give you a headache.

Against this backdrop, this article covers the following:

- How does inventory financing work?

- Reasons to get inventory financing

- Advantages and drawbacks of inventory financing

- What costs are involved in inventory financing?

- Alternatives to inventory financing

How does inventory financing work?

Definition

Inventory financing is a form of asset-based loan or line of credit (LOC) made available for you to purchase inventory.

In inventory financing, there is no need to pledge your company’s property or equipment as collateral. Instead, the loan will be collateralized by the inventory that you purchase. In the event of default, the creditor will seize and sell your inventory to make up for the outstanding balance.

Types of credit facilities

Inventory financing unlocks access to two types of credit facilities: a loan or line of credit. Inventory loans and line of credits are both secured by inventory, but they are structured in different ways.

1. Inventory line of credit

An inventory line of credit gives you access to a pool of funds, which you can use as needed and repay later. Unlike inventory loans, interests are only charged on the amount you use.

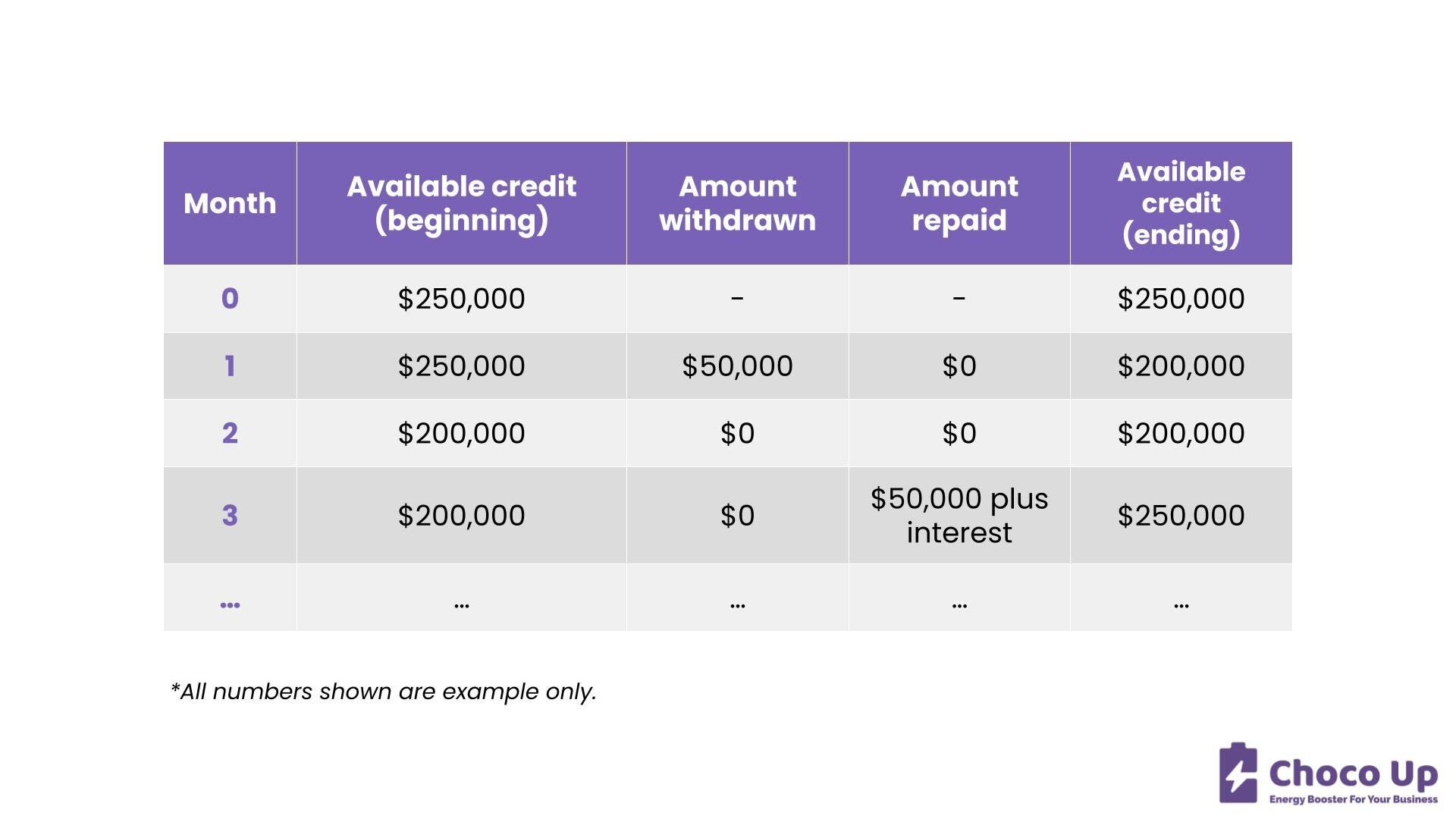

Inventory lines of credits are often revolving, which means that once you have repaid what you borrowed, that amount will be available for you to use again (see Month 3 in the example below).

Inventory line of credit example

- Appraised value of inventory: $500,000

- Credit limit: 50% of inventory value

- Interest rate: 10%

In this example, the credit limit is $500,000 * 50% = $250,000. In other words, you can use up to $250,000 in your line of credit. Interest will be charged at 10% on the amount borrowed.

2. Inventory loan

In an inventory loan, you will be given a lump sum of money to finance your inventory purchase. You will then pay back the amount, with interests, over a period of time.

Inventory loan example

- Appraised value of inventory: $500,000

- Loan amount: 50% of inventory value

- Interest rate: 8%

- Loan term: 24 weeks

In the example above, you will be given $500,000 * 50% = $250,000 for your inventory purchase. You will then repay the amount, with interest, over a period of 24 weeks.

Reasons to get inventory financing

Mostly sought by product-based businesses, inventory financing is helpful as a source of capital for inventory purchase.

Here are some common scenarios in which inventory financing may be needed:

- Your company just received a massive order from a client. Without adequate cash on hand, you need extra money for inventory purchase.

- Similar to scenario #1, someone just placed a huge order at your company. Cash reserves are sufficient to complete fulfillment. Yet, you wish to fund the bulk purchase with outside money in order to maintain a strong liquidity position for your business.

- You are expecting a significant increase in sales volume (e.g. festive seasons, summer months, holidays etc.). To prepare for the increased demand, you need money to purchase large amounts of inventory.

- Your company just made a bulk purchase of inventory. As a lot of capital is tied up in the goods, your business experiences a short-term cash flow gap.

Advantages and drawbacks of inventory financing

Pros

- Unlike traditional bank loans where you need to provide valuable business assets as collateral, the only collateral in this type of financing is your inventory.

- Applying for business loans (especially bank loans) could be painstakingly tedious. Provided that your inventory records are well-organized, inventory financing would be much easier to apply.

- For startups, small and medium-sized enterprises (SMEs) and other companies without strong credit histories, your business credit may not be a barrier to funding.

- Inventory lines of credit allow you to withdraw funds on an as-needed basis. There is no need to apply for a loan every time your business needs money.

Cons

- Creditors would not lend more than what your inventory is worth. The loan amount usually ranges from 20% to 65% of your inventory’s appraised value.

- As there are no ‘valuable’ business assets to secure the loans, inventory financing is deemed high risk by lenders. Interest rates are therefore set higher to compensate for the increased risks.

- In addition to charging higher interest rates, creditors may also require automatic repayment to minimize default risks. In other words, the cash generated from sale of goods goes directly to repaying the loan.

- In the financing agreement, creditors may specify certain rules (known as “loan covenants”) that you must comply with.

For example, you may be asked to take out insurance policies on collateralized inventory. You may also be required to use the borrowed funds for inventory purchase only.

- Prior to granting an inventory loan or line of credit to your business, due diligence may be conducted on your company.

Common due diligence procedures include review of accounting systems, field examination of warehouse facilities, testing of inventory systems, appraisal of inventory, etc.

For borrowers who need large amounts of funds, due diligence could be extensive and expensive. - Inventory loans are short-term in nature. Therefore, installment payments tend to be large, putting your business under huge financial pressure when paying off debts.

- Whether you have the financial capacity to repay an inventory loan depends largely on whether you can sell the goods that you purchase.

Inventory financing could be risky if your company’s upcoming sales performance is unpredictable.

What costs are involved in inventory financing?

As with any business financing method, the costs of inventory financing vary from lender to lender. Your company’ financials may play a part in determining the costs, too.

Here are some common cost items for your reference:

| Costs | Explanation |

| Origination fees | Typically assessed at a percentage of the loan amount, origination fees are charged by lenders for processing your loan application and setting up the loan. |

| Appraisal fees | Sometimes known as inspection fees, appraisal fees are charged as the lender inspects your goods, appraises the value of inventory and reviews your inventory management system. |

| Interests | Interests are charged on the amount borrowed. |

| Prepayment fees | You may be charged prepayment fees if you make repayments earlier than as stipulated in the loan agreement. This is to compensate the lender for lost interests on the prepaid amounts. |

| Late payment fees | If you fail to repay on time, late payment fees may be incurred. |

Alternatives to inventory financing

Inventory financing could be costly. If you have the door open for other financing solutions, here are some alternatives to consider:

Invoice financing

Similar to inventory financing, this is a form of asset-based financing.

To obtain funding, you could sell outstanding business invoices at a discount, or use your invoices as collateral for a loan or line of credit.

However, invoice financing and inventory financing share the same major drawback, namely, interest rates are high and a handful of fees may be charged.

Bank loans

Traditional bank loans operate in the conventional way. Bank lenders provide you with a lump sum which you will repay with interests.

Bank loans are repaid in fixed installments in accordance with a predetermined schedule. While this arrangement gives you a clear picture of your company’s contingent financial obligations, the flip side is a lack of flexibility — scheduled repayments could be rough on you during slow months.

Revenue-based financing (RBF)

Compared with loans, revenue-based financing gives you much-needed flexibility in repayment.

In revenue-based financing, RBF platforms (such as Choco Up) give you a lump sum, which you will repay through a portion of your company’s revenue. No dates are set as to when you need to repay a fixed amount of money.

Revenue-based financing also comes with relatively low cost of capital, as only a one-off flat fee is charged for obtaining RBF funding. There are no interests or hidden fees.

Learn more:

- E-commerce Financing: Options to Finance Your Online Business

- E-commerce Funding: A Guide to Your Options

- E-commerce Lending: Loan Options and Alternatives

- Merchant Cash Advance (MCA): Everything You Need To Know

Finding the right funding partner

Financing decisions can make or break your company. Finding the right funding partner could help you monetize valuable opportunities and accelerate growth, whereas ill-suited financing solutions could put your business in a debt trap.

Choco Up believes that flexibility is a crucial aspect of funding solutions for fast-growing companies. During periods of rapid growth, the last thing you want is to have debt commitments holding you back from spending on your business.

Choco Up therefore offers revenue-based financing, a flexible and non-dilutive funding solution, to high-growth startups, SMEs and e-commerce companies. They do not require regular fixed sum repayments, nor do they take equity from your company.

With Choco Up‘s ‘grow now, pay later’ approach, businesses benefit from growth funding today, repaying only with a small portion of their revenues later. To learn more about how Choco Up could help your business grow, check out their client success stories or apply for funding now!

About Choco Up: Founded in 2018, Choco Up is the leading revenue-based financing platform in Asia Pacific, offering non-dilutive growth capital to fast-growing companies.

Currently covering more than 10 markets and 10 sectors, Choco Up has helped hundreds of businesses capture growth while protecting equity upside.

Click here to apply for RBF funding!

Boxful Fulfillment X Choco Up Special Offer

Ready to drop a bomb? Don’t forget the essential key to a successful business, let Boxful Fulfillment handle your orders with accuracy and speed, amaze your customer with a better shopping experience. Get exclusive Choco Up customer fulfillment offer now.

*Partnership content from Choco Up.